SEC comments on non-GAAP metrics - are litigation-related adjustments misleading?

In the past year SEC issued comments to companies that eliminated litigation expenses in deriving the non-GAAP metrics. SEC comments led to changes in how companies calculate the metrics.

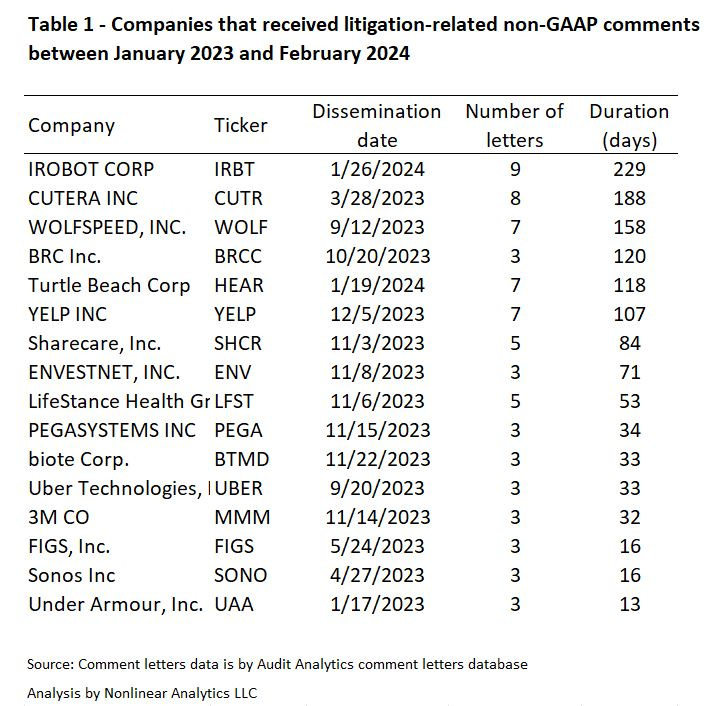

The Securities and Exchange Commission (SEC) commented on disclosures of at least sixteen companies between January 2023 and February 2024, seeking clarity about the types of legal costs removed at arriving at non-GAAP metrics.

Companies operating in litigious environments are prone to incurring legal expenses in the ordinary course of business. While companies can remove unusual legal gains and losses in presenting metrics not defined under GAAP, adjusting for normal and recurring legal costs is prohibited by Question 100.01 of C&DI’s that were updated on December 13, 2022.

Importantly, in contrast to comments that request more disclosure, SEC comments that cite Question 100.01 challenge how metrics are calculated. Say it differently: SEC comments may force companies to change their non-GAAP accounting practices and present different (usually lower) non-GAAP numbers to investors.

Additionally, non-GAAP comments that question litigation-related adjustments could shed light on changes in legal contingencies – an area of accounting where GAAP limitations allow companies to obfuscate disclosure of the amount and timing of legal accruals. (See discussion of Uber’s legal contingencies by Francine McKenna and me.)

In this blog, I discuss disclosure characteristics that raised SEC concerns, types of legal costs companies exclude when arriving at the non-GAAP numbers, and the outcomes of SEC non-GAAP comments.

Let’s look at the descriptive statistics of SEC non-GAAP litigation-related comments in Table 1 below.

Common characteristics of the companies that received litigation-related non-GAAP comments are:

Involvement in a mix of routine and non-routine legal cases;

A high impact of litigation charges on the non-GAAP bottom line;

A generic title of the non-GAAP line that does not specify which cases are excluded in the non-GAAP calculations.

Uber’s and 3M Co’s SEC comments illustrate the magnitude of the litigation charges. Uber’s (Ticker: UBER) “Legal, tax, and regulatory reserve changes and settlements” adjustment improved the fiscal 2022 Adjusted EBITDA by $732 million, or more than 8%. Similarly, 3M CO’s “Net costs for significant litigation” item improved the 2022 Adjusted Net Income of $5,777 by $1,815 million, or more than 30%.

Let’s turn to the specifics of SEC comments. For the most part, companies resolved SEC comments promptly in one or two rounds of back-and-forth comments. The average number of days to resolve the comments (the duration) was 86 days.

The examples of non-routine non-GAAP adjustments included the following items:

Expenses related to regulatory investigations. For example, Envestnet (Ticker: ENV) excludes “non-recurring legal and lobbying expenses” related to an FTC inquiry.

Costs of company-specific legal cases that have limited precedent elsewhere. For example, Uber excludes litigation costs related to classifying drivers as independent contractors versus employees.

Environmental and/or asbestos costs. For example, 3M CO (Ticker: MMM) excludes respirator mask/asbestos, PFAS-related, and Combat Arms Earplugs legal costs.

Acquisition-related and a class-action lawsuit legal settlements - for an example, see SEC comments to Sharecare, Inc. (Ticker: SHCR).

For companies that operate in industries where patent-related litigation is common and ordinary, excluding IP legal costs could potentially violate Regulation G.

Let’s look at the comments of the IROBOT CORP (Ticker: IRBT). SEC issued comments to IROBOT on May 11, 2023, seeking more clarity about whether IP litigation expenses are normal, recurring, cash operating expenses that should not be eliminated based on Question 100.01 of C&DIs:

We note you exclude IP litigation expense, net from Non-GAAP Operating (Loss) Income, Non-GAAP Operating Margin, Non-GAAP (Loss) Income and Non-GAAP Net (Loss) Income per diluted share. Since it appears legal costs are normal, recurring, cash operating expenses, it is not clear how you determined that eliminating these expenses from non-GAAP performance measures is appropriate or complies with Question 100.01 of the Division of Corporation Finance’s Compliance & Disclosure Interpretations on Non-GAAP Financial Measures.

IROBOT responded on May 25, 2023, that it considers SharkNinja’s litigation non-routine because of “the size, scope, complexity and frequency of this litigation” and because “litigation of similar size and complexity to the SharkNinja litigations is infrequent for the Company.”

The SEC disagreed with IROBOT’s conclusion and requested that the Company refrains from eliminating IP-related legal costs in future filings (emphasis added):

Although, your litigation with SharkNinja may be unique because of its size and complexity, based on the nature of the litigation, it continues to appear to us that the related expenses are normal operating expenses. In this regard, based on the nature of your business and products and as noted in your response, IP litigation arises during the ordinary course of your business.

The Company agreed to remove the IP-related adjustment in future filings and provided the following disclosure in its August 8, 2023, 8-K filing:

Beginning in the three months ended July 1, 2023, we no longer exclude IP litigation expense, net from our non-GAAP performance measures.

Notably, IROBOT did not revise the previous periods that included the non-GAAP IP litigation adjustment – which, for the six months ended July 1, 2022, was standing on $3.922 million. Say it differently, the change in how the metric is calculated affected the period-over-period comparability of the non-GAAP numbers.

Moreover, the Company didn’t attribute the change in non-GAAP calculations to SEC comments or explain why the methodological change was implemented. As discussed in my blog with Calcbench, managers generally have no incentives to disclose SEC reviews.

Non-GAAP metrics are not defined under GAAP and are unaudited. Additionally, no rules prescribe how methodological changes in non-GAAP presentation should be disclosed to investors. This topic deserves a more thorough discussion as a stand-alone piece.

Interestingly, in contrast to IROBOT, which was forced to remove the IP litigation adjustment, Sonos Inc (Ticker: SONO) was able to convince the SEC that Google/Alphabet IP legal expenses did not incur in the normal course of business:

In determining whether expenses directly related to the Company’s Alphabet/Google IP Litigation do not constitute normal, recurring, cash operating expenses necessary to operate a registrant’s business, the Company considered the following factors:

• While the related costs have been incurred over an extended period of time, they represent a single, discrete matter specific to the Alphabet/Google IP Litigation that is affecting a multi-year period and is distinct from the litigation, including IP litigation, that arises in the ordinary course of business for the Company.

• Due to the size of the counterparties and the extent of widespread infringement of the Company’s patents, the Alphabet/Google IP Litigation is outside the ordinary course of business on the basis of magnitude of the scope of litigation, as well as complexity of the cases. The litigation embodies the Company’s initiative to hold Alphabet/Google accountable for infringing more than 200 of the Company’s patents – a highly unusual level of misappropriation by one of the largest companies in the world, and which reflects Alphabet/Google’s wholesale copying of the wireless home audio experience that the Company pioneered and which remains at the core of its business. The potential damages the Company might recover from the litigation ranges [***] but is separate and distinct from the Company’s ongoing normal recurring, cash operating expenses necessary to operate its business. Moreover, the litigation is of such a complex, unusual, and important undertaking that the Company’s General Counsel obtained the Board of Directors’ approval before initiating legal action and provides an update to the Nominating and Corporate Governance Committee every quarter, as well as reports to the full Board of Directors. The litigation is also a regular subject covered during quarterly earnings calls.

Sonos also noted that costs of other IP legal cases are ordinary and are not included in the non-GAAP litigation line:

The Company further notes that legal costs that are determined to be normal, recurring expenses necessary to operate its business are not excluded when calculating Adjusted EBITDA. For example, the Company incurs in the ordinary course of business IP litigation expenses in a variety of matters other than the Alphabet/Google IP Litigation, and these expenses are deemed normal, recurring operating expenses and are not excluded when calculating Adjusted EBITDA (meaning not included within the “legal and transaction related costs” adjustment). Additional legal costs that the Company generally considers to be normal, recurring operating expenses, include, but are not limited to, recurring fees relating to trademark, antitrust, commercial litigation, regulatory compliance, data privacy, real estate, and labor and employment matters.

The difference in the outcomes of IROBOT’s and Sonos’ SEC reviews underscore that there is no one-fit-all solution. Companies should be mindful of their specific set of circumstances. Arguably, understanding how other companies addressed SEC comments should be helpful in efficiently responding to SEC inquiries.

Finally, a brief note about non-litigation non-GAAP adjustments challenged by the SEC on the grounds of being normal, recurring, cash operating expenses. Generally, the SEC objected to the exclusion of the following costs (note that these are examples and not a comprehensive list):

Pre-opening costs eliminated by retailers;

Compensation expenses and bonuses payable in cash (please note that historically, the SEC rarely challenged non-GAAP non-cash deferred compensation expenses);