Uber's Legal Contingencies - Can SEC Inquiries Add Clarity to "Unprecedented" Legal Charges?

Legal contingency balances are fraught with limited disclosure and substantial unforeseen charges. Is Uber telling investors everything?

The SEC issued a comment letter to Uber (UBER) on July 23, 2023, requesting additional clarity regarding its inclusion or exclusion of specific charges in its "certain legal, tax, and regulatory reserve changes and settlements" adjustment. Uber used this adjustment to calculate Adjusted EBITDA, a non-GAAP metric. Uber responded that the non-GAAP adjustments cover charges that are unprecedented in terms of “magnitude and timing” (emphasis added):

““Certain legal, tax, and regulatory reserve changes and settlements are primarily related to significant legal proceedings or governmental investigations related to worker classification definitions, or tax agencies challenging our non-income tax positions. These matters have limited precedent, cover extended historical periods and are unpredictable in both magnitude and timing, therefore are distinct from normal, recurring legal, tax and regulatory matters and related expenses incurred in the Company's ongoing operating performance.”

Uber is not the only company that says it makes non-GAAP adjustments for only the most significant non-routine adjustments, while excluding smaller charges. For instance, prior to the first quarter of 2022 Pfizer (PFE) had a policy of excluding only the amortization of intangibles related to large mergers or acquisitions. In Q1 2022, Pfizer revised this policy to include the amortization of all intangibles.

However, in the case of Uber, the SEC’s comments specifically address legal contingencies—an area of accounting notorious for limited disclosure and substantial unforeseen charges. According to ASC 450, a loss contingency should be accrued if it is both probable and reasonably estimable. If a material contingency is possible but not probable, companies are required to disclose it but are not obligated to record an accrual in their financial statements.

Yet, companies have long argued that providing detailed loss estimates for each litigation contingency could divulge confidential information and potentially influence the outcome of legal proceedings. As stated in PwC’s guide:

“ASC 450 does not provide specific guidance as to the level of disclosures required (that is, individual contingency or some other aggregate level). However, it requires that reporting entities disclose information to keep the financial statements from being misleading.”

And also:

“One way to alleviate some of this tension is to aggregate losses. The SEC staff has accepted this approach, which enables users to have sufficient data, but does not provide such specific information that it could prejudice a legal matter.”

Non-GAAP adjustments and SEC comment letters on the topic could offer incremental information that ASC 450 allows companies to hide or obfuscate based on an absence of specific detailed disclosures.

Let's begin by examining Uber's aggregated disclosures from its Commitment and Contingencies footnotes of 10-K and 10-Q filings.

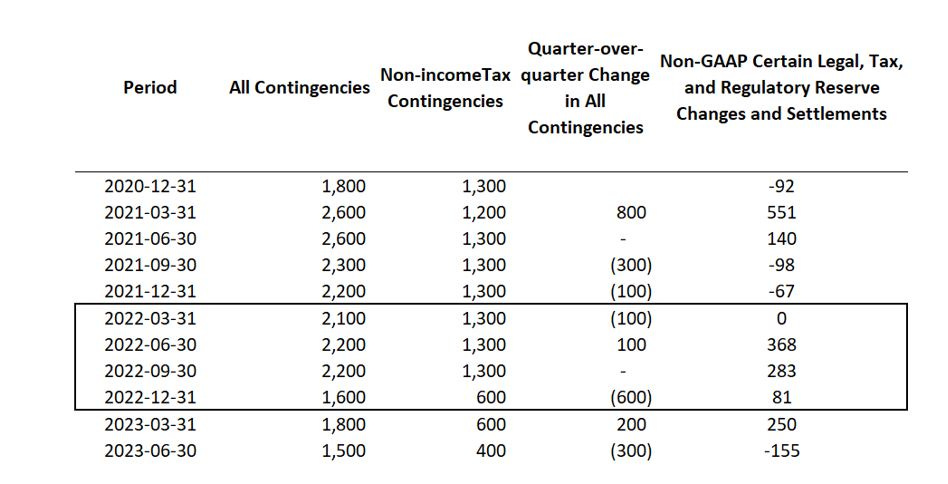

Table 1 – Uber’s Legal Contingencies and non-GAAP Legal, Tax, and Regulatory Reserve Disclosure, million $:

(Source: Uber’s 10-Q and 10-K filings and non-GAAP disclosure from 8-K filings)

All Contingencies and Non-Income Tax Contingencies (a subset of all contingencies) data was collected using Calcbench’s XBRL Data page and manually spot-checked. We begin the analysis in the last quarter of 2020 because this is the first period for which the breakdown between All and Non-Income Tax Contingencies was available. We primarily focus on 2022 because that was the period reviewed by the SEC.

As we can see from the table, All Contingencies and Non-Income Tax Contingencies were practically flat between Q1 and Q3 of 2022 and were standing on $2.1 billion, $2.2 billion and $2.2 billion, respectively, for All Contingencies, and $1.3 billion for each quarter for the Non-Income Tax Contingencies.

The $600 million decline in All Contingencies and $700 million decline in Non-Income Tax contingencies in Q4 2022 were likely related to the resolution and settlement of a dispute with UK tax authorities concerning VAT remittance. The expected impact of the dispute was fully accrued as of the third quarter ending September 30, 2022, with payment made in Q4 of 2022:

“On October 31, 2022, we resolved all outstanding HMRC VAT claims related to periods prior to our model change on March 14, 2022. We do not expect any significant impact to our statement of operations as we have adequate reserves recorded as of September 30, 2022, related to this resolution. We expect a cash outflow of approximately GBP 615 million during the fourth quarter of 2022 for this resolution.”

As permitted by ASC 450, Uber does not disclose when the GBP 615 million accrual was initially recorded and does not attribute the remaining $600 million in Non-Income Tax Contingencies to any specific cases or jurisdictions.

Additionally, aside from the UK settlement, the high-level footnote disclosure provides limited information regarding intra-year changes in the contingency account balances. The "certain legal, tax, and regulatory reserve changes and settlements" line in the Adjusted EBITDA metric (last column in Table 1) offers slightly more detail.

It might be worth pausing to explain how the accounting works. All Contingencies (and its subset of Non-Income Tax Contingencies) is a balance sheet account that shows the total amount of money that Uber accrued (set aside) for future settlements. The balance sheet contingencies increase when a company sets more money aside and decreases when the balance is reversed (for instance, when settlements are paid or if a company decides that future settlements are likely to be lower than initially anticipated).

The non-GAAP line, on the other hand, is an income statement (expense) account that represents additional accruals recorded during the quarter. Logically, we should, for the most part, expect a positive relationship between the changes in the period-end accruals and the non-GAAP litigation expenses (in case of Uber, between columns 4 and 5 in Table 1). Periods with cash payments of already accrued amounts, such as Uber’s Q4 payment, are an exception because cash payment is not an expense.

Now let’s look at the numbers. While Uber's non-GAAP disclosure highlights substantial accruals of $368 million and $283 million in Q2 and Q3 of 2022, respectively, period-end balances of All Contingencies were flat at $2.2 billion. Logically, for the account to remain flat, Uber had to make offsetting entries to reduce contingencies by approximately the same $368 and $283 million. The GAAP and non-GAAP disclosures do not provide sufficient information to understand what that offsetting entry could be or to trace the $368 and $283 million charges back to specific litigation or regulatory sanctions.

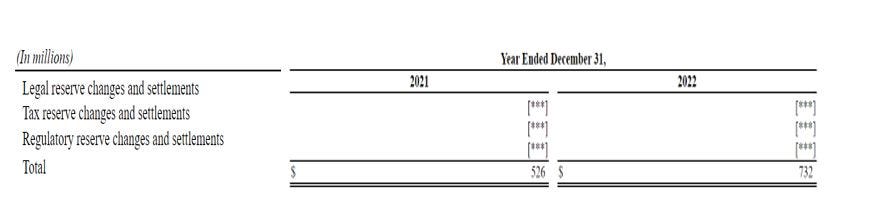

The SEC's comment letter should add to our understanding. Unfortunately, although Uber provided a breakdown of charges between the legal, tax and regulatory categories, the numbers are redacted in its response to the SEC.

The Commission's Rule 83 (17 CFR 200.83) permits companies to withhold portions of their responses to the SEC, often to protect proprietary information from competitors. However, information valuable to competitors is likely of interest to investors and journalists as well. In essence, by filing a request for confidential treatment, the company signals the importance of this information.

So, what can we glean from the unredacted, publicly available portions of the comments?

First, SEC comments underscore the lack of comparability between GAAP and non-GAAP contingencies. While non-GAAP contingencies related to non-routine cases totaled $732 million in 2022, GAAP charges (which encompass all changes in legal, tax, and regulatory accruals) are likely to be higher.

Second, Uber's response indicated that during 2022, the company identified three legal, three non-income tax, and six regulatory matters as "non-ordinary." Although we cannot attribute specific amounts to individual cases, the information suggests that Uber has "non-ordinary" unresolved non-income tax cases in at least three jurisdictions. (Please note that this assumption may not hold if all accruals related to the UK VAT issue were made in prior years.)

| A guest post by

|

“Lies, damned lies and adjusted EBITDA.”

- Mark Twain