Recent SEC Comment Letters Point to Continued Accounting Scrutiny

Recent restatements and ICFR revisions attributed to comment letters suggest that SEC scrutiny continues even as public comment-letter activity remains below historical levels.

In the past several weeks, Francine McKenna and I spent considerable time analyzing SpaceX IPO filings, including an analysis of changes between the confidential Draft Registration Statement (DRS) and subsequent public filings on Form S-1, under the presumption that some of the disclosure changes could be attributed to SEC review of the SpaceX registration filings.

Both Francine and I may say more about SpaceX accounting in the future – see also our additional posts here and here. In this post, however, I wanted to step back and look at a different corner of the SEC comment-letter process – namely, routine reviews of periodic filings such as 10-Ks and 10-Qs.

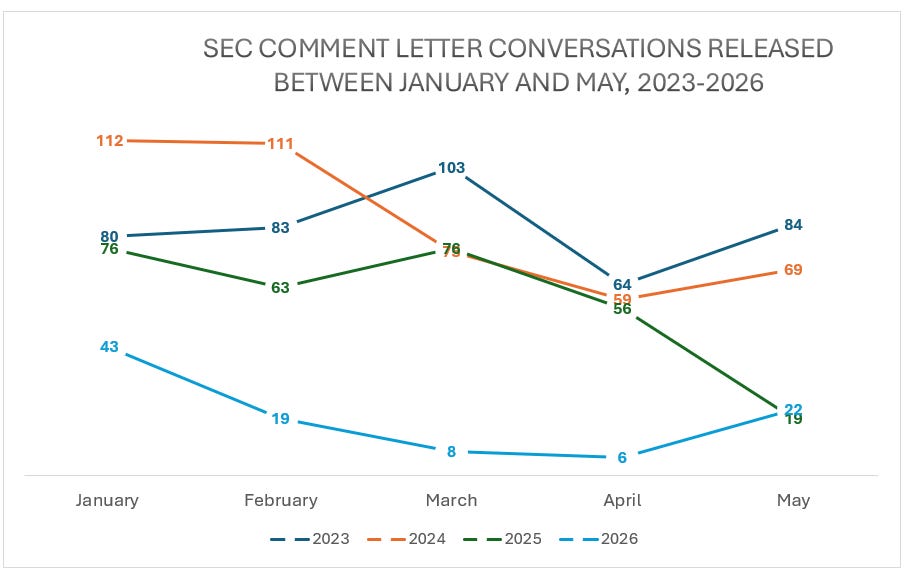

SEC comment letter activity, at least as measured by the number of letters publicly released on EDGAR, remained materially below historical levels in the past year. That decline appeared to be attributable to slower review activity following the October–November 2025 government shutdown and staffing disruptions within the Division of Corporation Finance, which led to fewer comment letters issued and even fewer disseminated.

The prior trend of declining number of SEC comment letters released on EDGAR continued into the first half of 2026, with only 8 and 6 conversations with a closing letter released in March and April, respectively, and 19 conversations released in May 2026, according to my analysis of data by Audit Analytics.

Source: Ideagen Audit Analytics Comment Letters Database, analysis by Deep Quarry.

However, several recent filings disclosed restatements and internal control over financial reporting (ICFR) weaknesses directly tied to the SEC comment letter review process, suggesting that SEC scrutiny is still ongoing behind the scenes. Importantly, the underlying SEC correspondence for some of those cases has not yet been released on EDGAR. In other words, even though investors are still seeing fewer comment letters on EDGAR, we can see traces of SEC enforcement and disclosure oversight elsewhere in public filings.

At the same time, some of the comment letters that have been released over the past several months appear interesting — for instance, because they question unusual non-GAAP charges or repeated accounting estimate revisions.

In this piece, I will discuss the SEC comments to four companies:

SEC comment letter to JetBlue Airways (Ticker: JBLU), seeking clarity on the materiality of changes in accounting estimates related to useful lives and residual values of JetBlue’s aircraft;

Century Aluminum Company (Ticker: CENX) consolidation-related Big R restatement triggered by SEC comments;

MINERALRITE (Ticker: RITE) acquisition-related Big R restatement triggered by SEC comments;

New Century Logistics (Ticker: NCEW) amended ICFR report, filed to address SEC comments.

SEC Comment Letter to JetBlue Airways

On March 31, 2026, the SEC issued comments to JetBlue Airways Corporation (Ticker: JBLU), seeking clarity on JetBlue’s revisions to aircraft useful-life and residual-value estimates tied to the company’s “capital-light growth” strategy. The Staff noted that JetBlue had extended the estimated useful lives of certain Airbus A320 aircraft in recent years — from approximately 25 years to as much as 36 years — while also revising residual-value assumptions and delaying dozens of future aircraft deliveries.

The SEC requested expanded disclosure regarding:

The number of aircraft affected by the revisions in each fiscal year;

How the aircraft were selected for estimate revisions;

The quantitative impact of the changes in estimates on depreciation expense, net income, and EPS under ASC 250; and

The Company’s underlying materiality analysis in support of its conclusion that the effects were not material.

SEC comment letters can provide supplemental information, such as context for substantive disclosure changes, that is often unavailable elsewhere in the public domain. While companies may decline to answer analysts’ questions or avoid discussing sensitive accounting judgments in detail on earnings calls, issuers are generally required to respond to SEC comments. As a result, the correspondence process can reveal the SEC’s concerns, management’s accounting rationale, and areas of disagreement or uncertainty that are not otherwise visible to investors.

At the same time, many SEC comments are relatively routine and ultimately result only in modest disclosure clarifications or immaterial wording revisions. For that reason, not every comment letter is equally informative. I tend to pay closer attention to SEC comments that invoke ASC 250, Accounting Changes and Error Corrections, because those comments often question potentially material changes in accounting estimates, revisions in methodology, or questions regarding whether prior disclosures adequately explained the nature and impact of accounting changes.

Please note that I am neither saying nor implying that all ASC 250 comments are triggered by wrongdoing. However, accounting changes generally require valid business or economic justification, particularly when they involve recurring estimate revisions or affect key financial metrics. When the SEC specifically requests that a company provide a quantitative and qualitative materiality analysis under ASC 250, that often suggests the change may have been material, whether from a pure accounting or a business and operational perspective. In other words, even when the immediate numerical impact appears relatively small, the underlying rationale and disclosure context of the accounting change could still provide incremental information to investors.

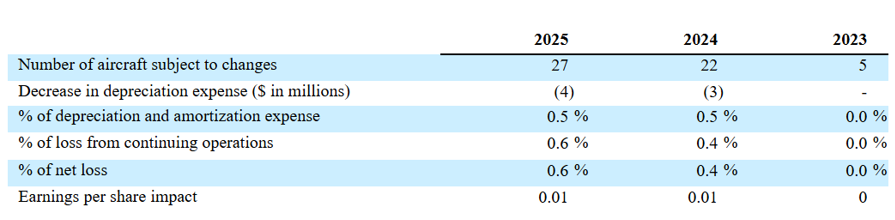

In its April 10, 2026, response to the SEC, JetBlue provided details of the number of aircraft affected by the changes in estimates and addressed the accounting impact of the changes:

Source: JetBlue’s response to SEC comments, filed as a CORRESP filing dated April 10, 2026.

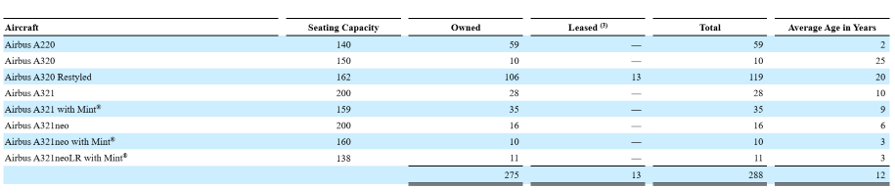

First, let’s look at the % of the aircraft affected. The change in the estimated useful lives and residual values primarily affected A320 aircraft, according to JetBlue’s disclosure. As of December 31, 2025, JetBlue had 229 A320 aircraft in its fleet, with the average age of 20 to 25 years:

Source: JetBlue’s 10-K for the year ending December 31, 2025.

During the three years ending December 31, 2025, JetBlue extended the useful lives of 54 aircraft, or about 24% of the A320 aircraft and 19% of the total fleet. Arguably, this change is material from the fleet management and liquidity perspective. However, from an accounting perspective, the change appeared to be immaterial, decreasing expenses and increasing net loss by 0.5% and 0.6%, respectively, in 2025.

So, how is an extension of useful lives of a substantial portion of the fleet from 25 years to 30-36 years immaterial to the financial numbers? The reason relates to how accounting estimates change under ASC 250 work in practice. Changes in useful lives and residual values are applied prospectively rather than retroactively. In other words, JetBlue did not reverse prior years’ depreciation. Instead, the remaining undepreciated carrying value of each aircraft was reallocated over the newly revised remaining useful life.

That distinction matters because many of the affected A320 aircraft were already relatively old — in many cases, roughly 20–25 years into service. By December 2025, a substantial portion of the aircraft’s original cost had already been depreciated. As a result, even a significant extension of remaining useful life — for example, from 25 years to as much as 36 years — would only spread a comparatively small remaining book value over additional years. Consequently, the prospective reduction in annual depreciation expense was economically meaningful from a fleet-planning and liquidity perspective, yet comparatively modest from a near-term GAAP earnings perspective.

SEC comment letters to JetBlue were publicly released on EDGAR on May 22, 2026.

JetBlue is not the only airline whose aircraft depreciation estimates attracted SEC attention. In March 2024, the SEC issued a comment letter to Southwest asking the company to explain how it established the 25-year useful life and 13%–20% residual values for its aircraft, how it periodically revisited those assumptions, and how it considered the marketability of used aircraft affected by FAA grounding and Boeing safety concerns:

“We understand from your disclosure that you estimate the useful life of flight equipment at 25 years, and associated residual values that range from 13% to 20%.

Please explain to us how you established the useful lives and residual values of your aircraft, and describe any efforts undertaken to revisit and update these policies on a regular basis. For example, given your disclosure on page 52, that you own 736 Boeing 737 aircraft, tell us how you considered the potential effect on marketability of used aircraft that were subject to the FAA grounding discussed on page 42, to address manufacturing and safety concerns, in estimating residual values and disposal costs.”

Southwest responded to the SEC by explaining that aircraft useful-life and residual-value estimates are based on historical operating experience, projected utilization, maintenance considerations, and independent third-party valuation data. The company emphasized that the estimates are reassessed periodically and adjusted prospectively as aircraft approach retirement and management gains better visibility into expected disposition values, including whether aircraft will be dismantled for parts or sold intact. Southwest also argued that its historical experience of generally avoiding material gains or losses on aircraft disposals supported the reasonableness of its depreciation assumptions and estimate revisions.

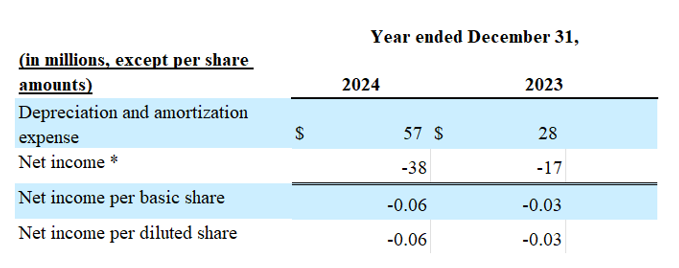

While we do not know why the SEC issued depreciation-related comments to Southwest, we do know that in both fiscal 2023 and 2024, Southwest revised the useful life of some of its aircraft to be retired early, which reduced Southwest’s EPS by (0.03) and (0.06) in 2023 and 2024, respectively:

“In 2024 and 2023, the Company identified certain -700 aircraft that were to be retired earlier than planned through 2025. This change in retirement dates, and the corresponding impact to depreciation expense, is considered a change in estimate and resulted in the following impact to expense in 2024 and 2023.”

Source: Southwest’s 10-K for the year ending December 31, 2025.

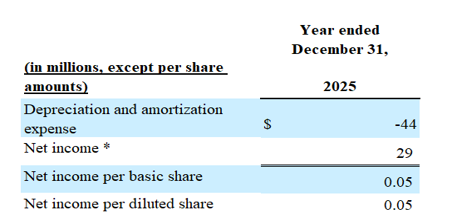

Additionally, Southwest revised the residual values of some of its aircraft in fiscal 2025, increasing the 2025 EPS by $0.05:

“During third quarter 2025, the Company completed an annual review of the estimated residual values of its long-lived assets. As a result of this review, the Company increased the estimated residual values for its Boeing 737-700 (”-700”) airframe and -700, Boeing 737-800 (”-800”), and Boeing 737-8 (”-8”) engine assets. This change took into consideration third party valuation data and recent market transactions. As this is considered a change in estimate, it has been accounted for on a prospective basis in accordance with Accounting Standards Codification (”ASC”) 205, “Accounting Changes and Error Corrections” and thus the Company will record less depreciation expense over the remainder of the useful lives for each related asset. This change in estimated residual values, and the corresponding impact to depreciation expense resulted in the following impact to expense in the year ended December 31, 2025.”

Source: Southwest’s 10-K for the year ending December 31, 2025.

Note that, in contrast to the change in estimate related to breakage revenue recorded in 2024, depreciation-related changes in estimates were not reflected in Southwest’s non-GAAP section.

To sum it up, changes in aircraft useful lives and residual values appear to affect multiple companies in the airline industry, with multiple revisions spread over several years. SEC comment letters and company’s responses may provide additional context to the reported changes.