Long SEC Reviews Quarterly Update # 5

Long SEC reviews reflect ongoing regulatory concerns over a company’s financial disclosures or accounting practices, signaling potential risks or uncertainties to investors.

What are unresolved SEC comments, and why are they important?

SEC comment letters refer to issues or concerns the U.S. Securities and Exchange Commission raised during the regulatory review of publicly traded companies' financial reports, particularly in their 10-K and 20-F filings. The routine reviews aim to enhance transparency, accuracy, and compliance in these companies' accounting and disclosure practices.

When the SEC identifies deficiencies or unclear aspects in a company's financial reports, it issues comment letters to request clarification or corrections. Companies are expected to address these comments promptly within ten business days of receiving the comments. The number of comments received, and the time taken to address them (duration) are often used as metrics in academic literature to evaluate the significance of concerns raised by the SEC (Cunnigham and Leidner, 2022). While SEC comments are typically resolved within 40 to 60 days and through one or two rounds of comments, some inquiries remain unresolved for an extended period, sometimes up to a year.

Companies are generally not required to disclose ongoing SEC reviews. However, "Item 1B Unresolved Staff Comments" of 10-K filings requires companies to report unresolved SEC comments issued at least 180 days before the fiscal year-end. This extended duration of unresolved comments could indicate more complex or significant issues that require additional time and effort to rectify (see further discussion of outcomes of unresolved SEC comments here).

Item 1B Unresolved SEC comments – quarterly update # 5 for the quarters ending December 31, 2024, and March 31, 2025

Two companies disclosed unresolved SEC comments during the March 31, 2025, quarter. There were no unresolved SEC comments disclosures during the December 31, 2024, quarter.

Custom Truck One Source, Inc. (Ticker: CTOS) disclosed on March 4, 2025, that the Company received SEC comments related to the presentation of Adjusted EBITDA as defined in the Company’s debt covenants. According to the Company, while the SEC did not object to the presentation of the measure as a liquidity metric, Staff did not believe that the presentation of the metric as performance was appropriate.

While the Company did not disclose why the SEC objected to the presentation of Adjusted EBITDA as a performance metric, Question 102.09 of SEC’s C&DIs requires that for a material agreement with a material covenant, a company discloses the measure used to assess compliance with the covenant as it appears in the debt covenant. (See an example here.)

Additionally, companies must reconcile their non-GAAP metrics to the most comparable GAAP numbers to avoid undue prominence in non-GAAP presentation. The SEC recently issued comment letters reminding several companies that the most comparable GAAP number for liquidity measures is cash from operations and not net income. (See examples here and here.)

The second company with Unresolved SEC Comments, Greenway Technologies Inc (Ticker: GWTI), disclosed on March 11, 2025, that the SEC requested that the Company amends its conclusion of Disclosure Control and Procedures to ineffective. As discussed in my previous update, the Company agreed to comply in future filings. SEC comments were publicly disseminated on EDGAR on October 13, 2023.

Longest SEC reviews and limitations of Item 1B Unresolved SEC Comments requirements

Item 1B disclosure is important because it alerts investors about material outstanding issues raised by the regulators while the review is ongoing and before SEC comments are publicly released on EDGAR. Yet, Item 1B has several limitations:

Companies are required to disclose unresolved SEC comments that were outstanding at least 180 days prior to the fiscal year-end. Suppose SEC comments were issued to a company with a calendar year-end in mid-July and were still outstanding as of the 10K date. The disclosure is not required in this case because the comments were outstanding for less than 180 days.

The disclosure is not required if the comments were resolved before the 10-K filing date—even if they were outstanding for more than 180 days at the fiscal year-end.

Smaller reporting companies - as defined by Rule 12b-2 of the Exchange Act of 1934 - are not required to provide Item 1B disclosure.

(A memo by Latham & Watkins provides a more detailed overview of the regulatory requirements.)

Long comment letter conversations point to a disagreement between the company and the SEC about accounting treatment or disclosure, sometimes leading to a restatement of financial statements. Even if a company succeeds in convincing the SEC that the accounting treatment is appropriate, these comment letters are worth reading because they may flag material issues and provide incremental information about the impact of the issues on important accounting or business metrics.

My analysis identified twenty-two companies with SEC conversations that went on for at least 180 days. The analysis was based on the population of NYSE and Nasdaq companies with stock prices of at least $5 at the dissemination date.

The hard-to-resolve topics included:

Accounting for and disclosure of crypto assets;

Revenue recognition practices;

Presentation of non-GAAP metrics that remove normal, recurring operating expenses or create tailored accounting measurements;

KPIs such as a definition of a non-operating studio for a fitness operator;

Restatements and related materiality analysis;

Segment disclosures.

I discussed several of the companies and topics in my previous posts. For instance, my previous analysis covered SEC comments to crypto companies. To recap, the SEC's reviews of crypto companies have been both broad and prolonged, reflecting the agency’s scrutiny amid the novelty and complexity of accounting for digital assets. Common issues included insufficient disclosure of risks related to crypto assets, revenue recognition practices, bitcoin impairments, and classification of crypto-related cash flows.

I’ve also discussed SEC comments to Archer-Daniels-Midland (Ticker: ADM). The focus of SEC inquiries appeared to be correcting the error in intersegment sales as an immaterial revision. Following the inquiries, the Company reported a second restatement of the intersegment sales and characterized the error correction as a material Big R restatement.

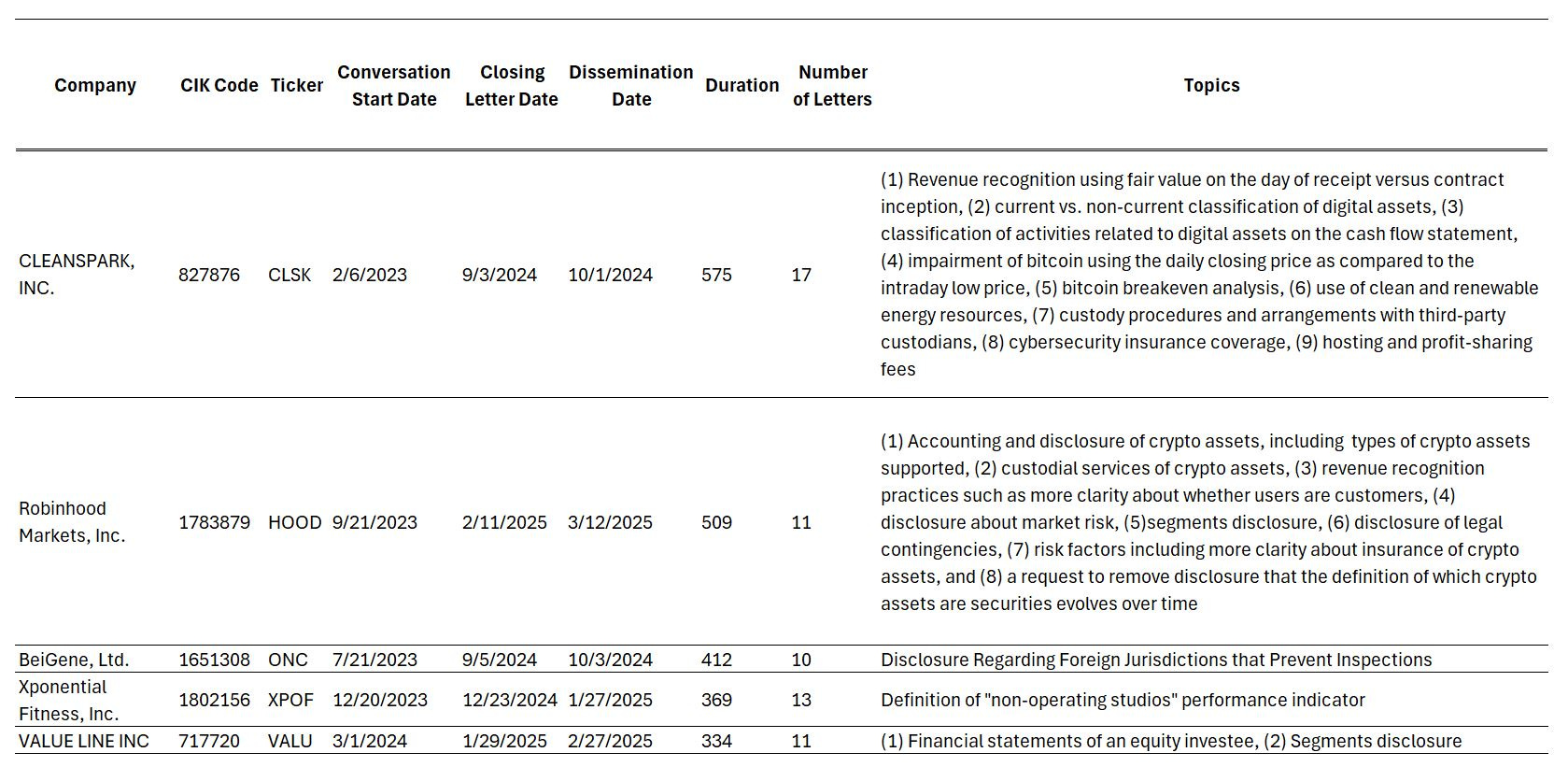

The table below reflects the five longest SEC comment letter conversations publicly released on EDGAR between October 1, 2024, and March 31, 2025.

Figure 1 – Longest SEC Comment Letters Reviews Releases on EDGAR between October 1, 2024, and March 31, 2025

CLEANSPARK, INC. (Ticker: CLSK) was the only company that disclosed unresolved SEC comments in its 10-K filing. The remaining companies did not provide Item 1B disclosure, likely because SEC comments were issued less than 180 days prior to the fiscal year.

Behind the paywall, I discuss SEC comment letters to Robinhood Markets, Inc. (Ticker: HOOD) and Xponential Fitness, Inc. (Ticker: XPOF) and explain why these conversations were hard-to-resolve.