Between Headlines and Numbers: AI’s Unanswered Questions

OpenAI’s uncertain IPO timeline, the turning tide of tokenmaxxing, the SEC’s questions about Oracle’s soaring capex, and different CAM approaches for data-center financing.

While most of my articles take a deep dive into a single story, the “Between Headlines and Numbers” series is a little different. It brings together several shorter notes — some based on in-the-news developments, others involve a brief follow-up on stories that I’ve written in the past, and a few sparked simply by items that caught my attention.

In this roundup, I’m highlighting three threads I’ve been following closely:

OpenAI’s reportedly shifted IPO timeline. A closer look at the timeline, the decision to file confidentially without a firm IPO date, and why OpenAI may be starting the SEC review process now while keeping the option to go public later — or sooner.

A turning tide of tokenmaxxing, and a growing disclosure question. Companies are reportedly spending billions on AI tokens, yet accounting and disclosure remain inconsistent and limited, making compute costs difficult to identify and compare.

The SEC comment letter to Oracle about soaring capex. The SEC issued comments to Oracle, asking to explain reasons behind its 209% capex increase.

Data center-related Critical Audit Matters (CAMs). Why Meta’s data-center financing arrangement resulted in a CAM while Oracle’s did not.

Source: Generated by ChatGPT.

OpenAI’s Reportedly Shifting IPO Timeline

I had an opportunity to speak with The Information about areas where I would like to see the SEC comment letter process focus on its review of OpenAI’s registration filings, including risk factors, related-party transactions, large off-balance-sheet commitments, and demand and supply risks:

“If I were to guess, the SEC will ask some questions about risk factor disclosures, business risks, demand and supply risks,” said Olga Usvyatsky, an accounting researcher who publishes a newsletter on regulatory developments.”

Why these areas? IPO registration filings are generally reviewed by the SEC staff, which may ask companies to revise or expand disclosures to add clarity or include material information before IPO proceeds. OpenAI has reportedly accumulated roughly $665 billion in future commitments, raising questions about the timing and enforceability of those obligations, the company’s ability to reduce or terminate them, and the consequences if future demand and related revenue fall short of current expectations. Put it differently: it’s a material risk, and risks need to be properly disclosed to investors.

Separately, OpenAI’s relationships with certain investors and strategic partners could raise related-party disclosure questions where those counterparties also transact with the company. For investors, the key questions include how much reported revenue may come from related parties, whether those transactions are conducted on terms comparable to third-party arrangements, and how dependent OpenAI’s growth may be on companies that also have an economic interest in its success.

The challenge for investors is timing. SEC comment letters and company responses generally do not become public until about a month — or, in some cases, even longer — after the registration statement becomes effective.

In our recent analysis of the SpaceX IPO process, Francine McKenna and I discussed another way investors may be able to identify potential areas of SEC concern before the letters themselves are released: comparing an initial draft registration statement, or DRS, with a subsequent public S-1 and examining where disclosure was added or revised. Academic research suggests that SEC reviews of registration statements can lead to economically meaningful disclosure revisions. However, investors generally cannot know with certainty whether a specific change resulted from an SEC comment until the correspondence becomes public.

There is an important caveat for OpenAI and Anthropic. That type of filings comparison requires access to public registration filings. Although both companies have publicly announced confidential submissions of draft S-1 registration statements to the SEC, neither draft prospectus is currently publicly available to investors.

For OpenAI, an interesting question may be when that public filing occurs. Under the SEC’s confidential-review process, a company pursuing an IPO must publicly file its registration statement and previously submitted nonpublic drafts at least 15 days before beginning a road show — or, if it does not conduct a road show, at least 15 days before the requested effective date of the registration statement. However, the timing of OpenAI’s IPO is uncertain.

On June 8, 2026, OpenAI announced that the Company filed confidentially with the SEC (emphasis added):

“We recently submitted a confidential S-1. We expect it to leak so we’re just announcing it. We have not decided on timing yet; it may be a while because there are things we want to do that are likely easier as a private company. But it’s a complicated set of tradeoffs and this gives us the option to go public sooner if that ends up being best.”

While WSJ initially reported that OpenAI seeks to go public as early as September, a later Forbes report, citing market volatility and valuation concerns, suggested a different timeline: the IPO may not happen until 2027.

OpenAI did not explain what it meant by activities that may be easier to pursue as a private company. Earlier reporting, however, suggests that the issue may extend beyond market timing. In April 2026, The Information reported that CFO Sarah Friar had privately questioned whether OpenAI would be organizationally ready for a 2026 IPO and whether slowing revenue growth could support the company’s roughly $600 billion of spending commitments. Separately, the WSJ reported growing concerns about supporting OpenAI’s data center spending, citing missed revenue targets.

Missing revenue targets may affect valuation and, therefore, is a valid reason to delay IPO. “Organizational readiness”, on the other hand, is a broad term that potentially covers financial reporting processes, internal controls, and the governance infrastructure required of a public company. While we do not have publicly available financial statements, it is not unreasonable to assume that OpenAI may go public with ineffective internal controls or less-than-perfect governance mechanisms — just as SpaceX and other IPO companies did. Yet, it is also reasonable to assume that it might be easier to fix the ineffective processes while the company is still private, away from public scrutiny.

Regardless of whether OpenAI ultimately lists in late 2026 or early 2027, the timing raises a separate question about how the company is using the confidential review process. Companies that completed IPOs often moved from the initial public S-1 to the offering within a matter of a few months: Loughran and McDonald (2013, JFE), for example, report a median of 88 calendar days between the initial S-1 filing and the IPO. Yet OpenAI submitted a confidential S-1 while explicitly saying that it had not decided when to proceed, that “it may be a while,” and that the filing gives it the option to go public sooner if that ultimately proves advantageous. OpenAI therefore appears to be seeking SEC review while preserving the ability to remain private for an undetermined period, rather than treating the confidential submission as the first step in a clearly timed offering.

OpenAI may not be alone in pursuing an SEC review well before a clearly scheduled offering. Anthropic confidentially submitted draft S-1 on June 1, while The Wall Street Journal reported that the filing could put the company on a path to go public in the fall, depending on market conditions. Even an early-fall offering would leave several months between the initial confidential submission and the IPO — potentially longer than the 88-day median between the initial public S-1 filing and the IPO reported by Loughran and McDonald.

Traditionally, the IPO process has been viewed as time-sensitive, in part because favorable market windows can open and close quickly. Generally, once a company decided to pursue an offering, it worked through SEC comments, seeking to reach the market while the IPO window remains open. A recent SpaceX IPO is an example of this approach.

Confidential submission reduced some of the risk of that process by allowing companies to begin SEC review without publicly committing to an offering and, if market conditions deteriorated, to withdraw without public visibility. Academic research has accordingly described confidential filing as a “de-risking” provision of the JOBS Act and found that firms facing higher proprietary disclosure costs were particularly likely to use it (Dambra, Field, and Gustafson, 2015, JFE); subsequent research similarly notes that confidential filers can abandon an IPO without leaving public record of withdrawal (Amaya et al., 2022, IRFA).

OpenAI appears to be approaching the process somewhat differently. Rather than filing confidentially as the first step toward a clearly timed offering, the company appears to have started SEC review well in advance of a firm IPO date, preserving the option to remain private while also positioning itself to accelerate if an earlier listing becomes attractive. Anthropic may be following a similar path, although the evidence is less explicit.

AI Costs Disclosure

Reports of rapidly rising corporate AI usage costs are becoming more common, but those costs remain difficult to see in financial statements. Recent reports that Meta and Uber have moved to limit employee AI usage after costs rose sharply provide an opportunity to examine where those expenses are recorded, whether they are large enough to affect reported cost trends, and what, if anything, companies disclose about them to investors.

The disclosure gap is particularly notable because companies frequently discuss the benefits of AI in considerable detail. For Meta, those benefits are two-fold. The company has highlighted AI-related improvements in its products, including content recommendations, engagement, and advertising performance, that are expected to support revenue growth and monetization. It has also pointed to significant internal productivity gains from AI tools.

As Meta explained during its Q4 2025 earnings call:

“We speak a lot about how AI is improving our products, but I’d like to take a moment to give an update on how it’s changing the way we work. Mark mentioned our focus on making Meta a place where individuals can have significant impact. A big focus of this is to enable the adoption and advancement of our AI coding tools, where we are seeing strong momentum. Since the beginning of 2025, we’ve seen a 30% increase in output per engineer, with the majority of that growth coming from the adoption of agentic coding, which saw a big jump in Q4. We’re seeing even stronger gains with power users of AI coding tools, whose output has increased 80% year-over-year. We expect this growth to accelerate through the next half.”

The ongoing operating cost of producing those benefits is much less visible. Disclosure of AI-related capital spending is far from perfect — for example, I have previously discussed the limitations of construction-in-progress (CIP) disclosures and the difficulty of determining how much construction spending relates specifically to AI infrastructure.

The operational costs of the AI productivity revolution are just as obscure. Usage-based AI expenses — including token-priced model access and other variable compute AI expenses — are often difficult to trace because they may be recorded across income-statement categories without being separately identified as AI costs.

A recent The Corporate Counsel blog, citing a memo from Troutman Pepper Locke, highlighted the disclosure dilemma. In particular, The Corporate Counsel noted that the shift toward token-based pricing can turn AI from a relatively predictable software expense into a variable, usage-driven cost. As consumption grows, those costs may become relevant not only for expense classification but also for MD&A, particularly when they materially affect margins, liquidity, or known trends and uncertainties, according to the memo.

The article also raises the possibility that economically similar AI costs may appear in different income statement lines depending on how the technology is used, with some companies recording the expenses as R&D costs while others reporting them as general and administrative expenses:

“The accounting — and disclosure — may be different industry by industry or company by company:

Different companies may account for AI token costs differently. For example, some companies may account for token costs in costs of revenue, while others may account for them as general and administrative (G&A) costs. For other companies, AI token costs might be accounted for research and development (R&D) expenses. For example, AI has started to significantly affect biopharmaceutical and biotechnology companies by rapidly transforming the drug development process, enhancing and speeding target identification, molecular design, clinical trials optimization, and regulatory processes — these companies are likely to record AI token costs as R&D expenses.”

Of course, companies are not required to disclose every category of operating cost; materiality matters. But, using Meta as an example, the potential scale of Meta’s AI usage costs makes the question worth asking.

According to The Information, an internal Meta memo said the company was likely spending billions of dollars on internal AI usage in 2026. Separately, SemiAnalysis estimated that Meta consumed roughly 70 trillion tokens per month in February and described the implied cost as close to $50,000 annually per employee at list prices. The SemiAnalysis figure should be treated as an estimate rather than Meta’s actual cash spending, particularly because negotiated pricing and the mix of models used could materially affect cost. Still, both estimates point to operating costs that may be large enough to warrant a closer look at what investors can — or, in many cases, cannot — see in the financial statements.

Meta’s own filings illustrate the disclosure limitations. The company says higher R&D expenses partly reflect infrastructure costs associated with its AI initiatives, while higher cost of revenue reflects increased data-center and technical-infrastructure operating costs (emphasis added):

“Cost of revenue in the three months ended March 31, 2026 increased $2.65 billion, or 35%, compared to the same period in 2025. The increase was primarily due to higher operational expenses related to our data centers and technical infrastructure…

Research and development expenses in the three months ended March 31, 2026 increased $5.55 billion, or 46%, compared to the same period in 2025. The increase was primarily due to increases in employee compensation, mainly driven by an increase in share-based compensation expense, as well as higher infrastructure costs for research and development, including our AI initiatives.”

The filing does not establish that the reported employee AI-usage costs are included in these infrastructure amounts, or identify where such costs are recorded. As currently disclosed, the expense disclosure is not sufficiently disaggregated to determine how much Meta spends on token usage or other consumption-based AI costs, whether those costs are increasing year-over-year, and, if so, by how much.

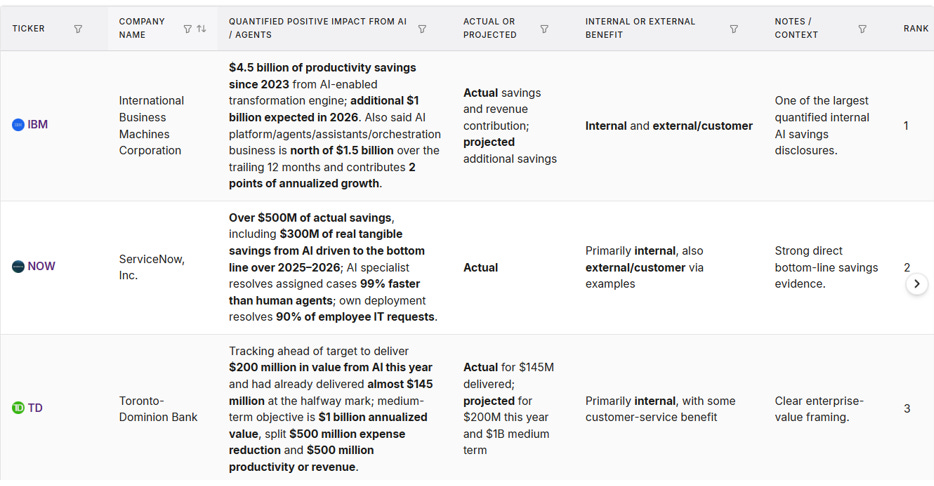

While I use Meta to illustrate the disclosure gap, the issue may be much broader. Hudson Labs recently published a research note, observing that companies such as IBM, ServiceNow, and TD Bank have quantified a range of AI-related benefits, including productivity gains and cost savings:

Source: Hudson Labs.

Kris Bennatti, the CEO of Hudson Labs, also highlighted this analysis in an X comment.

AI-related benefits identified in Hudson Lab’s post are likely to have a long-term positive effect on the bottom line. But can we reconcile the numbers behind those productivity gains or understand how those cost savings were calculated? The operating expenses associated with AI usage are often far harder to identify in financial statements than the benefits companies attribute to AI.

The problem of aggregated expense disclosure is not new. In 2024, the FASB issued a new standard, ASU No. 2024-03, Income Statement — Reporting Comprehensive Income — Expense Disaggregation Disclosures (Subtopic 220-40): Disaggregation of Income Statement Expenses, requiring public companies to provide greater disaggregation of expenses included in certain income-statement captions, responding to longstanding investor demands for better visibility into what drives the costs. The new requirements begin taking effect for annual periods beginning after December 15, 2026. Yet the standard may do relatively little to answer the AI-cost question: its required categories focus on items such as employee compensation, inventory purchases, depreciation and amortization — not token consumption or other usage-based AI expenses.