SEC comments on Free Cash Flow metrics - which adjustments are prohibited?

SEC comments on Free Cash Flow metrics - which adjustments are prohibited?

Over the past five years, the SEC flagged over a hundred companies with insufficient FCF-related disclosure. In many cases, SEC requested that companies remove or modify the FCF metric.

Free Cash Flow (FCF)—a non-GAAP metric typically defined as cash from operations less capital expenditures (CAPEX)—is one of the key financial metrics used by investors and analysts to gauge a company's financial health. It indicates the amount of cash available for distribution to shareholders, debt repayment, or reinvestment in the business.

The importance of the free cash flow metric implies that investors need to understand how the metric is calculated, which adjustments are included, and, if the definition of the metric changed from the previous period, what triggered the change.

Nicola White reported for Bloomberg on May 1, 2024, that the SEC’s Corp Fin repeatedly flagged companies that presented non-GAAP metrics that overshadowed GAAP results or were misleading:

“Companies and auditors have heard the SEC repeatedly warn against overplaying unofficial results and minimizing GAAP results, including through staff guidance in 2022 that also told companies not to remove normal, recurring expenses from their supplemental measures. Companies “should know by now,” said accounting analyst Olga Usvyatsky.”

Bloomberg’s article primarily focused on income-based metrics, such as Adjusted Net Income and EBITDA. Many compliance issues discussed by Bloomberg—such as presenting the most comparable GAAP number with less prominence or excluding normal and recurring business expenses—apply to all non-GAAP metrics, including the FCF. (In my February 21, 2024, piece, I highlighted types of adjustments that could be considered misleading.)

Yet, several issues specific to FCF warrant a more detailed discussion.

First, let’s look at the regulatory guidance. Questions 102.05 and 102.07 of SEC’s C&DIs address considerations specific to FCF:

While the FCF metric doesn’t have a uniform definition, companies should explain how the metric is calculated and reconcile it to the most comparable GAAP number;

Companies should not imply that FCF represents residual cash flow available for discretionary spending since many companies have non-discretionary expenses such as debt interest;

FCF is often used as a liquidity measure and, as such, must not be presented on a per share basis.

In addition, Item 10(e)(1)(ii) of Regulation S-K prohibits exclusion from certain non-GAAP liquidity metrics charges or liabilities that require cash settlement absent an ability to settle in another manner.

The guidance provided by Questions 102.05 and 102.07 was last updated in 2016, and Item 10(e) of Regulation S-K has been around even longer. So, companies had sufficient time to familiarize themselves with the guidance and, by now, should be fully compliant with the rules, right? Well, not exactly.

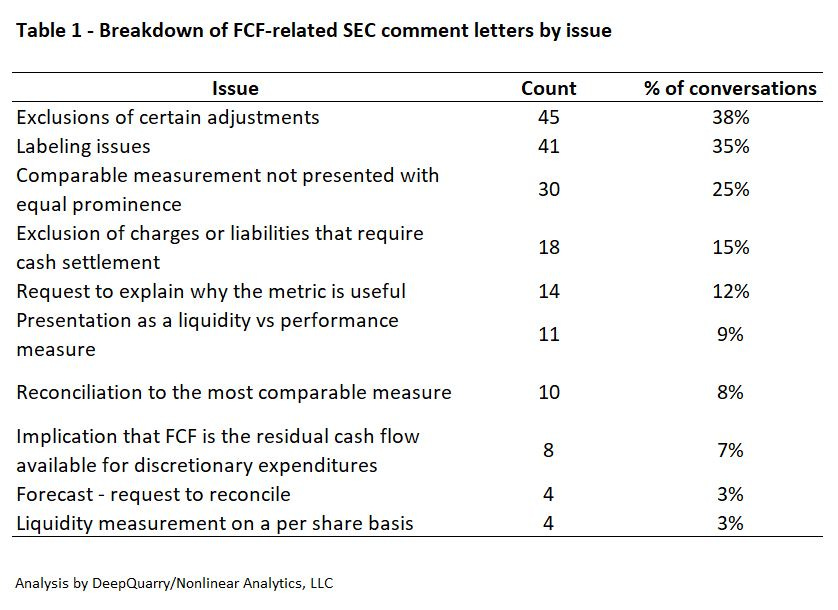

Based on my search in the Audit Analytics comment letters database, between January 1, 2019, and April 30, 2024, the SEC issued FCF-related comments to at least 116 companies.

Let’s look at the most common issues raised.

The following section provides a detailed discussion of selected categories, including specific examples.

Exclusion of certain adjustments

The most common concern raised by the SEC was the exclusion of disallowed adjustments. In contrast to comments that require more disclosure, questions about specific adjustments zoom into how the metric is calculated. Since most of the adjustments have a positive effect on the FCF, the concern is likely to be an overstatement of the metric. Say it differently: if the metric is modified following the SEC comments, the adjusted FCF bottom line will likely decrease.

The common types of concerns about the disallowed FCF adjustments included:

Adjustments that exclude charges or liabilities that require cash settlement in the absence of another settlement method, which are explicitly prohibited in liquidity measurements by Item 10(e)(ii)(A) of Regulation S-K;

Adjustments that remove normal, recurring, cash operating expenses from performance metrics pursuant to Question 100.01 of C&DIs;

Adjustments that create a tailored accounting method pursuant to Question 100.04 of C&DIs.

Roughly 40% of the questions that challenged specific adjustments did so based on a prohibition on excluding charges or liabilities that require cash settlement and cannot be settled in a non-cash manner.

Let’s look at an example of SEC comments to Zoom Video Communications, Inc (Ticker: ZM) issued on September 28, 2022:

“We note that your measure of adjusted free cash flow excludes litigation settlement payments. Tell us how you considered Item 10(e)(ii)(A) of Regulation S-K, which prohibits the exclusion of charges or liabilities that require, or may require, cash settlement from a liquidity measure. Please explain or revise to remove such adjustment. “

In its response dated October 19, 2022, the Company argued that the litigation charge is not part of the Company’s ongoing operating activities and is useful to investors. However, in a follow-up letter, the SEC pressed on, and on December 2, 2022, Zoom Video agreed to remove the adjusted free cash flow metric in future filings:

“You state in your response to prior comment 4 that your presentation of adjusted free cash flow does not violate the prohibitions in Item 10(e)(1)(ii)(A) of Regulation S-K. However, this guidance specifically indicates that the exclusion of charges or liabilities that required, or will require, cash settlement, or would have required cash settlement absent an ability to settle in another manner, cannot be excluded from non-GAAP liquidity measures other than EBIT and EBITDA. As such, please revise to remove this adjustment.

In response to the Staff’s comment, the Company has removed adjusted free cash flow from the Q3 Form 10-Q and will continue to do so in its future filings.”

Changing how the FCF metrics are calculated following SEC comments is not uncommon—in more than half of the instances, the SEC’s concerns about specific adjustments prompted companies to remove or significantly modify the FCF measures. However, companies rarely disclose SEC comments and do not always explain why they elected to change the metric's definition or remove the non-GAAP measure. SEC comments can provide context and shed light on changes in presentation.

For examples of SEC comments that cited Questions 100.01 and 100.04, see SEC’s comments to Redwire Corp (Ticker: RDW) and SEC’s comments to Enfusion, Inc. (Ticker: ENFN).

Labeling issues, presentation of FCF without the most comparable GAAP measurement, and implications that FCF is the residual cash for discretionary spending

Question 102.07 of SEC’s C&DIs recognizes that the free cash flow metric does not have a uniform definition. Yet, companies typically define the FCF metric as cash from operations less capital expenditures. If the metric calculation includes additional adjustments, the metric should be labeled as “adjusted free cash flow” or similarly.

To illustrate, let’s look at SEC comments to Johnson Controls International plc (Ticker: JCI) released on EDGAR on March 21, 2024:

“Please revise the title of your free cash flow measure to adjusted free cash flow or similar description as your calculation differs from the typical calculation of cash flows from operating activities less capital expenditures. Refer to Question 102.07 of the Non-GAAP C&DIs.

Response:

The Company acknowledges the Staff’s comment and has revised the title of the Company’s free cash flow measure to “adjusted free cash flow” in the earnings release furnished on Form 8-K for the quarter ended December 31, 2023, and will continue to do so in future earnings releases furnished on Form 8-K.”

Additionally, Question 102.07 requires that companies present the most comparable GAAP metric – typically, cash from operations for the liquidity FCF metrics – with equal prominence. From SEC comments to CORNING INC /NY (Ticker: GLW), publicly released on EDGAR in March 2024:

“The bullet points on page 1 present core gross margin, core operating margin, and free cash flow without the most directly comparable GAAP measures. Please revise to present the most directly comparable measures prior to the non-GAAP measures in accordance with Item 10(e)(1)(i)(A) to prevent undue prominence.

The Company acknowledges the Staff's comment. In future earnings releases furnished on Form 8-K, the Company will present the most directly comparable GAAP measures prior to the non-GAAP measures in accordance with Item 10(e)(1)(i)(A) to prevent undue prominence. Specifically, on the measures referred to by the Staff in the Staff's comment, the Company will disclose gross margin, operating margin and cash flows from operating activities prior to core gross margin, core operating margin and adjusted free cash flow, respectively.”

Finally, Question 102.07 of the C&DIs states that companies should not imply that FCF is the residual cash flow is cash available for discretionary spending because many companies use cash available after CAPEX to pay non-discretionary expenses such as debt servicing costs.

From SEC comments to Permian Resources Corp (Ticker: PR) publicly released on EDGAR on August 23, 2022:

“We note that you disclose discretionary cash flow in your calculation of the non-GAAP financial measure Free Cash Flow. Please tell us how you considered Question 102.07 of the Compliance and Disclosure Interpretation on Non-GAAP financial measures which states Free Cash Flow should not be used in a manner that inappropriately implies that the measure represents the residual cash flow available for discretionary expenditures and revise your disclosure, as necessary.

Response: We acknowledge the Staff’s comment and note that in future earnings releases and filings with the Commission we intend to revise the line item to be labeled “Operating cash flow before working capital changes” instead of “Discretionary cash flow” to avoid any implication that “Discretionary cash flow” is residual cash flow that is available for discretionary expenditures. “

Presentation of FCF on a per share basis

Question 102.05 of C&DIs explicitly prohibits presenting liquidity measures on a per share basis. While C&DIs do not explain why the liquidity per share metrics are disallowed, they refer to Accounting Series Release No. 142, issued in 1973.

According to ASR No. 142, the cash flow per share presentation may overshadow EPS, a major performance metric. Additionally, according to ASR No. 142, FCF per share is difficult to interpret and irrelevant to investors.

Notably, all four companies in my sample that received the SEC’s comments about FCF per share presentation agreed to remove the metric from future filings.

SEC comments to GoDaddy (Ticker: GDDY), publicly released on EDGAR in May 2024, illustrate a typical FCF per share question.

“We note your presentation of free cash flow per share throughout the 2023 Fourth Quarter Earnings Presentation on your website. Please revise to remove this presentation as non-GAAP liquidity measures that measure cash generated must not be presented on a per share basis. Refer to 100(b) of Regulation G.

RESPONSE TO COMMENT 3: We acknowledge the Staff’s comment and respectfully advise the Staff that we have removed the disclosure of free cash flow per share in our 2023 Fourth Quarter Earnings Presentation as posted on our website and we will also omit the disclosure of free cash flow per share in future quarterly results presentation materials.”

For questions and data inquiries, please contact olga@deepquarry.com