Super Micro's working capital is under pressure, on top of all its other troubles

Super Micro was struggling to stay listed, fend off short-sellers, satisfy auditors and investigate itself. But now its working capital is under pressure and the disclosure leaves open questions.

This is collaborative effort, co-authored with The Dig the newsletter from Francine McKenna. If you value our work, please subscribe!

They say cats have nine lives. Super Micro Computer appears to be using several of them. The broader issue for Super Micro is that the various crises increasingly appear interconnected rather than isolated.

In the past several years, Super Micro has faced:

auditor resignations;

delayed filings;

material weaknesses;

governance concerns;

short-seller attacks;

C-suite departures, including recommendations to replace the CFO;

export-control scrutiny, regulatory investigations including SEC subpoenas;

customer-concentration risks;

and now criminal indictments of individuals tied to the company for AI hardware exports.

We’re going to briefly review the history of Super Micro’s troubles observed in the last few years, and then, after the paywall, we dig into Super Micro’s Cash, Accounts Receivable, and Inventory and review the corresponding metrics to make a comment on Super Micro’s acute “working capital and liquidity” challenge.

Background

The latest chapter began in March 2026, when the U.S. Department of Justice indicted three individuals — including a Super Micro co-founder and board member — for allegedly conspiring to divert advanced U.S. AI technology to China in violation of export-control laws. Although Super Micro itself was not charged, the indictment pushed the company back into a position of a public issuer facing escalating questions about oversight, controls, governance, and management credibility.

But the roots of the current crisis stretch back much further.

In August 2024, short seller Hindenburg Research published a highly critical report accusing Super Micro of accounting and governance failures, related-party issues, and problematic sales practices. Shortly afterward, the company delayed its annual Form 10-K filing and began assessing its internal controls.

The situation escalated dramatically in October 2024 when Super Micro’s auditor EY made a noisy resignation after only a short engagement and without issuing the fiscal year 2023 audit opinion. EY disclosed it could no longer rely on management or the Audit Committee — an extraordinarily serious statement to make. Accounting observers immediately interpreted the resignation as potentially indicative of deeper governance or compliance problems, triggering widespread speculation about possible SEC scrutiny.

Francine was quoted by Fortune magazine:

Accounting expert Francine McKenna told Fortune that the EY resignation went beyond the usual quiet exit auditors make when they slip away from an engagement. “There are noisy resignations and then there are resignations that bang a big giant gong—and this is as bad as it can get,” said McKenna, who authors The Dig newsletter.

In its resignation letter, EY wrote that it was no longer able to rely on management and the board’s audit committee, which is supposed to be made up of independent directors who oversee the company for the benefit of shareholders. “When you can’t rely on management, that’s bad,” said McKenna. “If you can’t trust the audit committee, there is something very wrong.

Former regulators and compliance professionals publicly suggested EY may have filed a Section 10A notice with the SEC. Whether EY filed a Section 10-A notice to the SEC in conjunction with its resignation has not been publicly confirmed. From The Dig:

Did EY file a 10A? That’s what Ms. Lynch is implying.

Section 10A of the Securities and Exchange Act of 1934 requires reporting by auditors to the Securities and Exchange Commission (SEC) when, during the course of a financial audit, an auditor detects likely illegal acts that have a material impact on the financial statements and appropriate remedial action is not being taken by management or the board of directors.

In November 2024, Super Micro hired BDO USA to replace EY in an effort to complete delayed filings and regain Nasdaq compliance. The company also formed a Special Committee supported by law firm Cooley LLP and forensic firm Secretariat Advisors to investigate Hindenburg’s and EY’s allegations.

In December 2024, the Special Committee largely cleared management and the board, concluding that there was no evidence of executive misconduct, no restatement was required, and the Audit Committee had acted independently. The Committee also specifically addressed export-control compliance, stating that it found no evidence that anyone at the company had attempted to circumvent export restrictions or knowingly divert products to prohibited jurisdictions.

The Committee also recommended replacing the CFO. Super Micro moved quickly to elevate Kenneth Cheung as the CAO and principal accounting officer but, according to Fortune, CFO David Weigand, who was expected to stay until a replacement is found, remains in the job more than 14 months and four quarters later. There hasn’t been an update on the search since. Weigand spoke with analysts when the company announced its third-quarter 2026 earnings results, and signed off on the 10-Q and the company’s internal controls.

The Committee’s conclusion regarding export controls and the propriety of the rehire activity led by Weigand is, in hindsight, especially notable because one of the individuals later indicted in the DOJ export-control case was co-founder and board member Yih-Shyan Liaw. He is a former senior executive who had previously left the company during earlier accounting-related scrutiny and then was rehired. The Special Committee had reviewed and effectively endorsed Weigand’s rehiring decisions, including Liaw.

The Committee also reviewed revenue-recognition practices, quarter-end sales activity, customer concentrations, delivery timing, returns, and warranty practices. Despite reviewing 52 sales transactions — including transactions highlighted by EY — the Committee stated that it did not disagree with the company’s revenue-recognition conclusions and found no evidence of a pattern of shipping incomplete products near quarter-end to accelerate revenue recognition.

Even after the internal review, regulatory pressure continued to build.

In February 2025, Super Micro disclosed that both the SEC and DOJ had issued subpoenas related to the Hindenburg allegations and delayed filings. At the same time, securities litigation and derivative lawsuits began accumulating. Management reiterated that the Special Committee had found no support for EY’s allegations, while emphasizing that the company was expanding its leadership team across finance, legal, compliance, and operations.

The company also disclosed changes to previously announced preliminary unaudited financial results for the quarter ending June 30, 2024, including additional inventory charges. Although management continued to assert that no formal restatement was required, no restatement does not equate to the absence of errors.

In August 2025, Super Micro revealed in its 10-K for the year ending June 2025 that the company still faced extensive unresolved material weaknesses in internal control over financial reporting. These included deficiencies involving:

information-technology general controls;

segregation of duties;

completeness and accuracy of financial-reporting information; and

related-party disclosure controls.

The remediation effort is massive. Super Micro disclosed broad ERP redesign projects, segregation-of-duties remediation, enhanced compliance programs, expanded review procedures, and major personnel changes across finance and compliance functions. Professional-service expenses surged as the company relied heavily on external auditors, consultants, legal advisers, and remediation specialists. Audit fees increased from $4.8 million in fiscal 2023 collected by Deloitte, to $8.6 million in 2024 and $8.1 million in 2025 collected by BDO.

Yet even after those efforts, the problems remained unresolved.

In its most recent 10-Q, as of March 2026, Super Micro disclosed that the same core material weaknesses identified in 2024 remained unremediated, including IT controls, segregation-of-duties conflicts, deficiencies in information completeness and accuracy, and related-party disclosure weaknesses. The company acknowledged that these weaknesses could increase the risk of unauthorized system access, data manipulation, and financial misstatements.

Export Control Issues and Internal Investigation

In a previous piece, Olga examined how the March 2026 DOJ indictment involving certain Super Micro employees and intermediaries raised broader questions about the company’s export-control oversight, customer relationships, and financial reporting risks.

Her analysis focused not only on the alleged diversion of AI servers to China, but also on the potential impact on Super Micro’s relationships with suppliers and customers, such as Nvidia and Oracle, in an environment of tightening export-control enforcement and increasing political scrutiny of AI infrastructure supply chains. Olga discussed how the issue potentially extends beyond the immediate legal exposure associated with the DOJ indictment and into broader commercial and operational questions: whether large AI customers may reassess supplier risk, whether suppliers may increase compliance expectations and oversight, and whether counterparties may become more sensitive to reputational and regulatory risks associated with export-control investigations.

The fiscal Q3 2026 earnings call following the indictment demonstrated how central the issue had become for investors. Analysts repeatedly questioned management about export controls, customer confidence, regulatory risk, and whether large AI infrastructure customers might shift business to competing server vendors. Questions also focused on whether the investigation could affect Super Micro’s relationships with key suppliers such as NVIDIA.

For instance, Ananda Baruah of Loop Capital explicitly asked whether customers could become “skittish” and shift purchases to competing AI server vendors in light of the export-control allegations. CEO Charles Liang responded that, based on the company’s communications with customers, he did not “feel a negative feeling” at that moment and emphasized that Super Micro continued to expand its customer base.

On the other hand, Victor Chiu with Raymond James asked, in no shy terms, whether the investigation could reflect Super Micro’s relationship with Nvidia:

Does the investigation, you know, around the, that may potentially impact, you know, your relationship with NVIDIA, you know, subsequently, you know, your allocation or supply of GPU and other components? Cause I think that's another really frequent point of concern that we get from clients these days is, you know, how that impacts your relationship and, you know, whether or not that's the dynamic there has changed at all.

Super Micro confirmed there was no change in the relationship and that it remains strong.

Management attempted to reassure investors that all customer relationships remained strong and that no restatement was expected. However, beyond confirming that the investigation remained ongoing, the company provided little substantive detail regarding the scope, findings, remediation progress, or expected timeline of the investigation.

Super Micro did, however, update in the May 12, 2026, 10-Q filing its disclosure regarding the ongoing SEC investigation by stating that it received an additional subpoena from the SEC Enforcement Staff on April 28, 2026:

On November 19, 2024, the Company received a subpoena from the U.S. Securities and Exchange Commission Enforcement Staff in connection with an investigation entitled In the Matter of Super Micro Computer, Inc. The Company continues to produce documents in response to the subpoena. The Company received another subpoena on April 28, 2026. The matter is too preliminary to form a judgment as to whether the likelihood of an adverse outcome is probable and we are unable to estimate the possible loss or range of loss, if any.

The updated language is important because, despite volumes of documents that the SEC had already requested and received so far, it has now asked for more.

Broc Romanek is a former staffer in SEC Corp Fin office of Chief Counsel and advisor to an SEC Commissioner. He is now a strategic advisor to law firm Cooley LLP. Romanek told us, “This is not unusual. Investigations tend to expand if SEC Enforcement finds something interesting.”

Former SEC Enforcement attorney Greg Bruch, now leading his own firm, agrees. “Oftentimes, the first subpoena is broad enough to encompass everything, so the successive rounds are memorialized in letters where the staff asks for things that were not previously produced. A second round of subpoenas may mean that the Staff has found a new area of inquiry that is not covered by the first wave.”

New “interesting” areas of inquiry for the SEC is not good news for Super Micro.

Super Micro’s Working Capital Challenge

Meanwhile, Super Micro’s current financial condition as of May 15, 2026, based on its results for the quarter ending March 31, 2026, presents what appears to be a working capital and liquidity challenge.

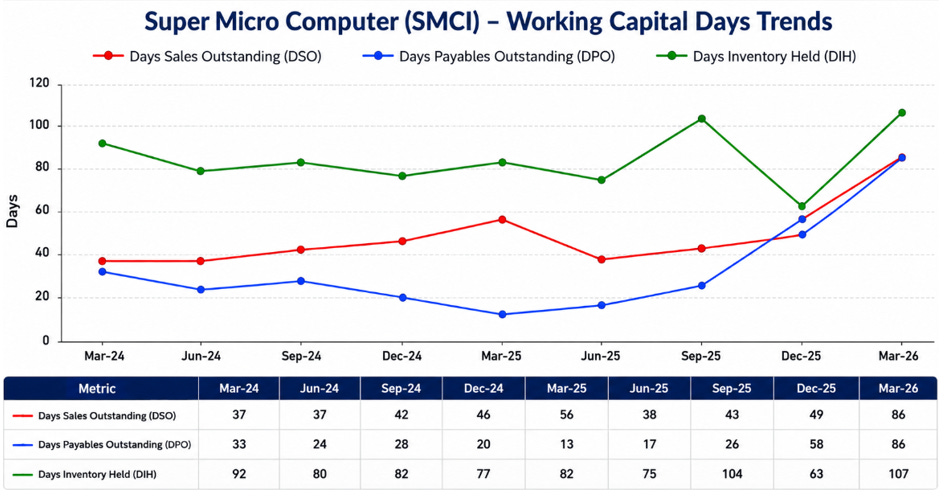

The chart below tells the tale.

Data source: Calcbench.

Days Sales Outstanding (DSO), a metric used to measure how quickly the credit sales are collected, rose from about 49 days in the December 31, 2025, quarter, to 86 days in the March 31, 2026, quarter, according to data from Calcbench. (Note that Calcbench relies on as-reported net account receivable balances to calculate DSO. The allowance for credit losses was $488 k and $0 at March 31, 2026, and June 30, 2025. )

Days Payables Outstanding (DPO), which measures how long it takes to pay suppliers, increased from about 58 days in December 2025 to 86 days in March 2026.

Days Inventory Held (DIH), a proxy for how long it takes to convert inventory into sales, remained elevated compared to historical levels, reaching 107 days in the March 2026 quarter.

After the paywall, we dig into Super Micro’s Cash, Accounts Receivable, and Inventory and review the corresponding metrics to make a comment on Super Micro’s acute “working capital and liquidity” challenge.