Post-mortem: The SEC's pre-IPO comment letters to SpaceX

Can investors infer the likely focus of the SEC’s confidential review before the comment letters become public? Yes! Yes they can!

This is collaborative effort, co-authored with The Dig the newsletter from Francine McKenna. If you value our work, please subscribe!

“[A]s we know, there are known knowns; there are things we know we know. We also know there are known unknowns; that is to say we know there are some things we do not know. But there are also unknown unknowns — the ones we don’t know we don’t know.” Former Secretary of Defense under George W. Bush, Donald Rumsfeld.

When SpaceX publicly filed its registration statement earlier this year, my friend and frequent collaborator Francine McKenna and I asked a simple question: Can investors infer the likely focus of the SEC’s confidential review before the comment letters become public?

To answer this question, we analyzed — in a newsletter published May 27, 2026 — the differences between the confidential draft registration statement (DRS) and the later public S-1. The premise was straightforward. Academic research suggests that SEC reviews frequently lead to economically meaningful disclosure revisions, but the comment letters themselves remain confidential until well after the IPO. By comparing the evolution of the registration statement, investors may be able to identify areas where the SEC likely requested additional disclosure or clarification.

The SEC has now released the SpaceX comment-letter correspondence, providing an opportunity to compare the disclosure changes we identified in our piece with the Staff’s actual comments. The usefulness of our approach, however, depends on one critical assumption: that a meaningful portion of the disclosure changes between the confidential DRS and the public S-1 were prompted by SEC comments rather than by the company’s own voluntary revisions.

Overall, the comparison suggests that our methodology held up well. The SEC prompted disclosure changes based on their comments and we can now see mirror changes to those identified in our analysis in a few key areas: discussions around the Monthly Active Users (MAU) metric, risk factor disclosures, shareholders’ rights, useful lives of PPE, and tax disclosures.

Equally interesting are the SEC comments that were not discussed in our analysis. Some, such as those related to revenue recognition, relate to disclosure changes that we omitted at that point because complex accounting topics warrant a separate later discussion while taking the context of the comments into consideration. Others could not have been inferred from the registration statement alone because they did not lead to a change in the disclosure.

Finally, those comments that could not have been inferred from the registration statement alone provide additional insight into how the Staff approached SpaceX’s offering. They illustrate both the strengths and the constraints of using draft-to-final filing comparisons to anticipate confidential SEC reviews.

In this piece, we want to come full circle on our earlier piece by examining the SEC’s comment letters, highlighting where the earlier analysis accurately anticipated — and in some cases predicted — the Staff’s concerns. We also discuss several noteworthy SEC comments that we did not discuss in our original piece.

Some of the key points we touch upon after the paywall:

How well did the DRS-to-S-1 methodology work? We trace the disclosure changes we identified in the original analysis to specific SEC comments — and examine where the approach worked well and where it could not have predicted the Staff’s concerns.

The MAU and KPIs debate. The SEC repeatedly questioned why SpaceX did not present MAUs and other KPI metrics.

AI business segment. Should SpaceX provide more granular disclosure?

Agreement with Anthropic. How much of the disclosure was added voluntarily?

Descriptive Statistics and Characteristics of the SEC Review

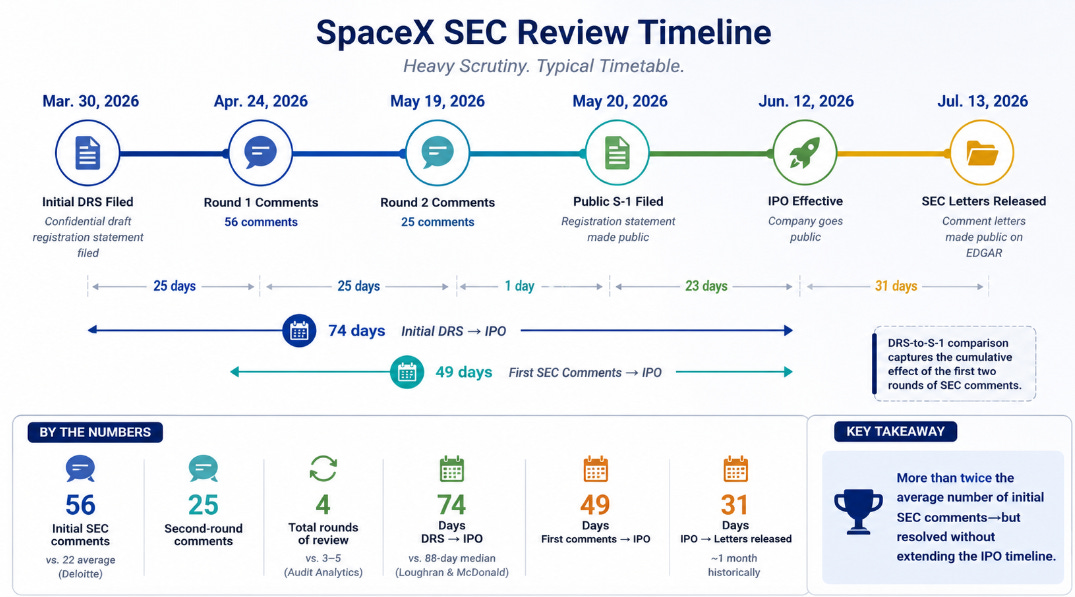

Before examining the substance of the SEC’s comments, it is useful to put the review process itself into context. By several measures, the SEC’s SpaceX review was more extensive than for a typical IPO, while other metrics were in line with averages.

SpaceX filed an initial DRS prospectus on March 30, 2026, and the SEC sent its first comment letter on April 24, 2026 — within the 30 calendar day timeframe advisors to pre-IPO companies expect.

SpaceX went public on June 12, 2026 — approximately 49 days after receiving its first SEC comments and 74 days after filing the initial DRS filing. The DRS-to-IPO time lag was within the range of SEC review described by Orrick. (Note that Orrick’s SEC review timeline includes 30-day pre-DRS consultation with the SEC. In our earlier piece we used 88 days from Loughran and McDonald, 2013, JFE. )

The SEC SpaceX correspondence involved four rounds of comments, consistent with Audit Analytics’ earlier findings that IPO reviews averaged between three and five SEC letters during 2016 through the first quarter of 2018. Deloitte likewise cautions that IPO registrants should expect several rounds of comments, although its recent analysis does not report a numerical average.

SpaceX SEC comment letters were publicly released on EDGAR on July 13, 2026 — 31 days after the IPO date. The SEC generally reviews all IPO registration statements, but the correspondence remains confidential until at least 20 business days after the effective date. Historically, IPO comment letters often became public within a month after the offering. More recently, however, release times have lengthened. For example, although Figma went public on July 31, 2025, its SEC comment letters were not released until September 25, 2025 — nearly two months later.

The volume of comments in SpaceX’s initial letter, however, was considerably higher than that of a typical IPO. The Staff raised 56 comments in the first round. Deloitte’s recent sample of 50 IPOs completed during the year ended July 31, 2025, averaged 22 initial comments, with a range from a handful to 45. SpaceX therefore received more than twice the recent average and exceeded the highest number observed in Deloitte’s sample.

At the same time, the extremely detailed review was not without precedent. As Francine McKenna noted in her analysis of Coinbase’s 2021 direct listing, Coinbase received 55 initial SEC comments, and earlier IPOs drew even more extensive first-round reviews:

The first letter from the SEC to Coinbase on December 7, 2020, based on the company’s first draft registration statement filed confidentially October 9, 2020, is a doozy! There were 55 comments! How does that stack up with others?

Francine also cited an Audit Analytics report, which noted that Aramark received 84 comments in its initial letter in 2013, while Alibaba’s F-1 attracted 86 comments in 2014.

SpaceX is not a typical IPO candidate. Its registration statement spans a highly complex business that combines satellite communications, spacecraft manufacturing, AI-related business, and a social platform X, all supported by a complex capital structure. For companies of this size and complexity, comparisons to the average IPO may be less informative than comparisons to other large, operationally complex offerings. Compared to other complex businesses such as Coinbase, the 56-comments initial letter may not look as unusual.

The rest of our analysis is behind the paywall. Won’t you consider subscribing?