Answering some questions about Tesla’s CAPEX

Recent writing about Tesla’s PPE spend seemed to raise more questions than it answered. We’ll try to remedy that.

This is collaborative effort, co-authored with The Dig, the newsletter from Francine McKenna. If you value our work, please subscribe!

At the request of some readers, we have added a summary of the post.

Tesla’s CAPEX: Understanding the Accounting Complexity

Introduction: Tesla’s recent capital expenditure (CAPEX) disclosures have raised questions among investors, primarily due to a perceived $1.4 billion gap between the company’s reported CAPEX spending on the cash flow statement and the change in its property, plant, and equipment (PPE) values on the balance sheet over the last two quarters of 2024.

This divergence prompted concerns about accounting transparency and whether Tesla’s investment in AI infrastructure is being accurately and fully disclosed.

Key Takeaways:

CAPEX Accounting Nuances: Companies, including Tesla, exercise significant judgment in determining when a new plant, for example, is placed in service and, therefore, when depreciation begins. Companies also have quite a bit of discretion in determining the useful lives of assets placed in service. These decisions impact the timing and extent of depreciation expenses and reported GAAP profitability. Decisions about when assets are placed in service and their useful lives may be a rational response to business conditions but can also obscure true financial performance.

AI-Driven CAPEX: Tesla’s significant AI-related investments—totaling approximately $5 billion in 2024—are central to its CAPEX profile. The company’s focus on AI infrastructure aligns it more with technology firms like Meta and Amazon than traditional automakers like General Motors (GM).

The $1.4 Billion GAP: The Financial Times highlighted a perceived discrepancy between Tesla’s reported CAPEX ($6.3 billion) and the change in its PPE value ($4.9 billion) for the last two quarters of 2024. Such a gap typically suggests timing differences, asset disposals, or non-cash transactions (like unpaid accounts payable).

Complex Explanations: Multiple factors may explain the gap, including:

Timing differences between cash outflow and asset recognition.

Unreported disposals of PPE assets.

Prepayments for AI hardware (e.g., Nvidia GPUs) that send cash out long before assets are received and recorded on the books.

Classification choices for certain PPE assets, such as AI-related infrastructure.

Non-cash impairment charges.

Broader Context: Comparing Tesla’s CAPEX to other AI-heavy firms (like Nvidia, Meta, and Amazon) reveals that such gaps are not unusual, reflecting industry-wide challenges in CAPEX reporting.

Investor Implications:

Transparency in CAPEX and PPE reporting is crucial for assessing a company’s true capital allocation efficiency.

For institutional investors, Tesla’s substantial AI-driven spending aligns with its technology-driven valuation but warrants close monitoring given the complexities in its financial disclosures.

The volatility in CAPEX reporting may present risks to earnings quality and financial clarity.

Conclusion: While Tesla’s CAPEX gaps have raised concerns, the company’s AI-driven strategy and unique accounting judgments require a nuanced view. Investors should monitor Tesla’s disclosures, particularly around AI spending and PPE accounting, to ensure a clear understanding of its capital allocation strategy.

Our detailed analysis is behind the paywall.

Today we are going to talk about some recent discussion regarding Tesla’s CAPEX spending. But first let’s start at the beginning, with understanding more about how companies use, and sometimes abuse, the judgment and discretion allowed when reporting on spending and depreciation expense for acquisition and disposal of property, plant and equipment assets.

Last week, my friend and collaborator Francine McKenna of The Dig and I discussed with Bloomberg how companies frequently change the useful lives of equipment, such as technology-related equipment like servers. That can have a significant impact on future non-cash expenses and net income.

Extending the depreciable lives of equipment may reduce depreciation expenses and boost profits – thus, in some cases, raising concerns of accounting manipulation – both Francine and I believe that changing the depreciation schedules can also be a rational response to changing business conditions:

Adjusting the useful life up or down isn’t necessarily a nefarious thing,” said Francine McKenna, an adjunct lecturer in accounting at Montclair State University…

…Lengthening the useful life of a factory, for example, makes sense when a business faces uncertainty and hesitates to allocate new capital resources for investments. “Then you see things stretching out because the company says, ‘I am going to hold on to this asset for longer,’” said Francine McKenna.

However, the depreciable life of equipment varies among industries or even within the same industry. I recently wrote how Amazon, citing AI innovation, decreased the useful life of a subset of servers from 6 to 5.5 years. On the other hand, Meta and Oracle increased the useful lives of their servers and networking equipment to six years.

According to Bloomberg, while operational differences could explain some of the differences in how long companies hold on to their equipment, the novelty of the AI servers contributes to the complexity of making the useful life estimates:

Widespread use of AI servers is a relatively new phenomenon, which means companies are still learning how best to account for them…

…even within the same industry, there can be different dynamics. Amazon, for example, reduced the useful life of its servers, while Facebook increased it. “It is possible to have different useful lives for identical servers, for instance because there are different workloads or more efficient data center designs,” according to Usvyatsky, the accounting researcher.

AI-related CAPEX spending is not limited to servers. According to CNBC, Meta, Amazon, Alphabet, and Microsoft intend to increase AI spending to $300 billion in 2025.

Tesla, on the other hand, alone spent about $5 billion on AI in 2024:

After its earnings report in late January, Tesla said AI-related capital expenditures were approximately $5 billion in 2024, out of $11.34 billion total. The company expects its AI spending to be flat year over year.

For accounting purposes, CAPEX, or "property plant and equipment" investment spend is capitalized on the balance sheet — rather than expensed on the income statement — and the asset is depreciated over its useful life. Thus, it's a reasonable assumption that reported CAPEX spending in a given year — based on disclosures and the PPE spend number that adjusts the accrual-based income statement to cash flows — would approximate the change in the gross (before depreciation) PPE balance on the balance sheet. But that’s an approximation that does not include certain transactions such as asset disposals and impairments which would reduce the asset balance.

A recent FT article noted that for at least one company — Tesla — this assumption fails by a wide margin, $1.4 billion in the most recent two quarters:

Compare Tesla’s capital expenditure in the last six months of 2024 to its valuation of the assets that money was spent on, and $1.4bn appears to have gone astray.

The FT article, by Wirecard sleuth Dan McCrum, compares Tesla’s $1.4 billion gap between the PPE purchased during the period, based on the adjustment number for year-end 2024 Statement of Cash Flows, and the change in the PPE balance on the Tesla balance sheet, to General Motors’s numbers.

According to the FT, GM's numbers match up:

Looking at last year, in the third and fourth quarter combined, Tesla spent $6.3bn on “purchases of property and equipment excluding finance leases, net of sales” according to its cash flow statements. Over on the balance sheet, however, the gross value of property, plant and equipment rose by only $4.9bn in that period…

…We’d expect the numbers to tally. General Motors, for instance, spent $30bn on capex over the past three years, disposed of $14bn of assets, and so reported a $16bn rise in the gross value of property, plant & equipment to $88.7bn at the end of last year.

In our view, it's not an apples-to-apples comparison to pit the change in Tesla's assets over only the last two quarters of 2024, against GM total activity over a three-year period. The more data you have, the more it tends to smooth out the timing differences between when cash goes out the door and when assets are recorded on the books.

Additionally, Tesla reportedly claims that about half of its investment in CAPEX is driven by its investment in AI infrastructure. Understanding AI spending and liquidity is crucial for companies such as Tesla, where rich valuations compared to peers are driven, in part, by the AI narrative story.

We believe the comparison group should include AI-heavy companies in addition to General Motors because spending on AI CAPEX may follow different payment patterns than non-AI machinery or equipment.

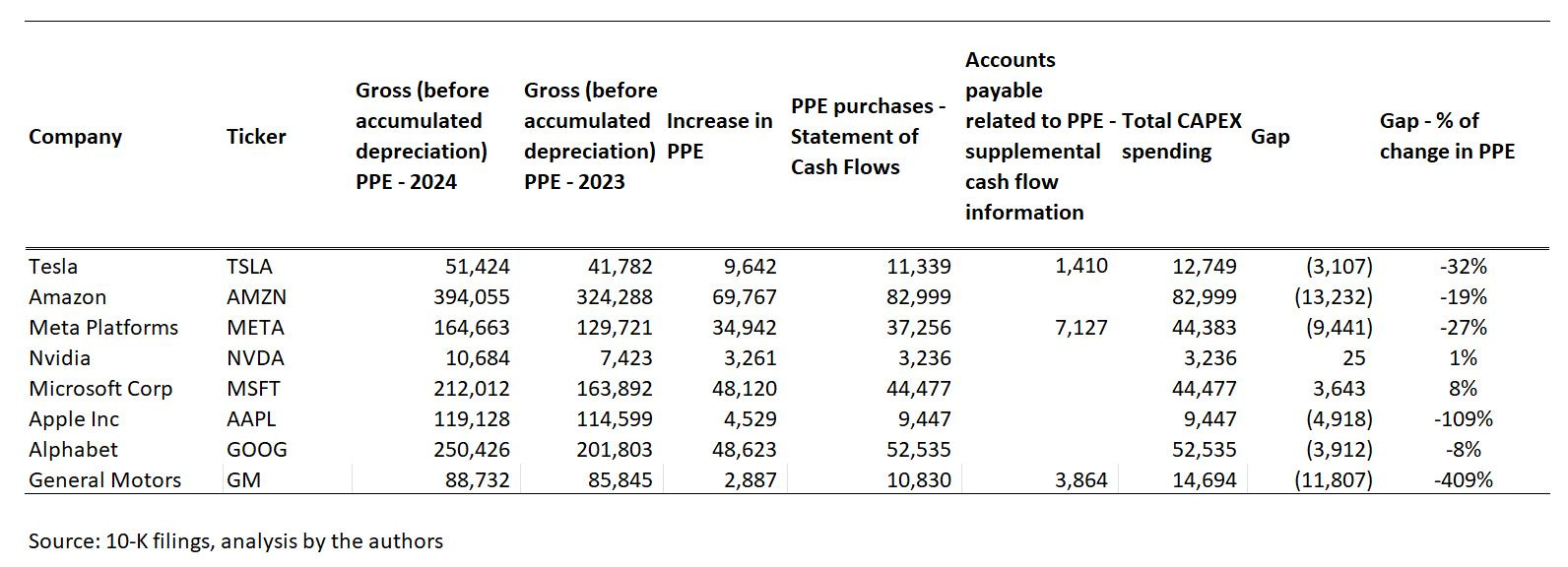

The figure below illustrates the "gap" between the changes in gross PPE and PPE spending reported on the Statement of Cash Flows for large technology companies with significant AI spending – known as the “Magnificent 7” — and General Motors.

Figure 1 - PPE gap for "Magnificent 7", millions $

A methodology note: PPE purchases are for the year 2024 and that gap is calculated as a comparison of asset change vs PPE spending.

Figure 1 shows that five companies in our sample have a large gap between the change in PPE values and CAPEX-related cash outflow over the same period. When we compare the same one-year unadjusted (before disposals or impairments) gap, Tesla does not appear to be an outlier. The notable exception in the sample is Nvidia, with a gap of about 1% for the year ending January 25, 2025.

A CNBC article explains why Nvidia may stand apart from the crowd:

Nvidia won’t report results until later this month. And its capex figures will look very different since Nvidia is the one developing and supplying AI technology rather than buying it.

The point here is that for NVIDIA, much of the AI-related technology it buys is for inventory, not PPE. Note also that we are looking at a one-year point in time data, so we cannot rule out that the nearly exact match for Nvidia is just a coincidence or a statistical fluctuation. For instance, the numbers may be very close because Nvidia did not have asset disposals or impairments during this particular year.

This raises another interesting question: if most companies have wide gaps at some point in time, is it still useful to try to reconcile Tesla’s PPE numbers? In our opinion, the analysis in Figure 1 underscores the across-the-board challenges in reconciling CAPEX spending, which the commenter in the FT article mentioned (emphasis added):

Luzi Hail, professor of accounting at the Wharton School, told us:

The reasons for why the reported numbers will not fully add up in most cases is that we only see the net changes in these accounts (i.e., PP&E and the associated Accumulated Depreciation accounts) but do not have all the detailed transactions that were going on. Maybe they sold off some PP&E and we do not know what the net book value (the respective gross amounts) were. Other things that will make an exact reconciliation impossible are M&A transactions and foreign currency transactions. So, in most cases, the capex number will give you a good approximation for the increase in gross PP&E but there could be other reasons going on for why in a particular case this might not be the case.

Tesla did not disclose any sales of PPE, impairments, or gains and losses from disposals of PPE during 2024. But that may be a disclosure decision, based on its judgment to combine what it considers non-material amounts from those activities on other lines of the income statement, balance sheet, and Statement of Cash Flows, not because they did not happen at all.

After the paywall, we explain how the “gap” should be calculated, using not only cash outflows but what remains in A/P, the downside of making the comparison between the cash flow numbers and the balance sheet “point in time” numbers, dismiss some other explanations for the Tesla gap that have been suggested, and offer what we believe is the most likely reason for Tesla’s apparent gap, as well as some other possible explanations for the ongoing discrepancies in Tesla’s financial reporting.