Under Armour corrects immaterial errors - is there more to the story?

Under Armour corrects immaterial errors - is there more to the story?

Under Armour corrected immaterial errors and disclosed an intent to reduce the compensation of current executives. Clawbacks and forfeitures after immaterial errors are rare and warrant more analysis.

Under Armour, Inc. (Ticker: UAA) disclosed in its annual report for the year ending March 31, 2024, that the Company identified immaterial errors in its previously filed financial statements for the annual and quarterly periods between January 01, 2021, and December 31, 2023, and revised its previously filed financial statements.

In the same filing, the Company also disclosed that, following the revision, it decided to forfeit part of the executive compensation voluntarily. Clawbacks after immaterial errors are rare—based on my preliminary analysis, as of March 15, 2024, only one company indicated that it recovered previously paid compensation after a restatement.

Naturally, the decision to clawback or forfeit compensation – especially voluntarily after immaterial errors - is not made lightly, so one may wonder whether there is more to the story.

According to the Company, the errors included the incorrect recording of:

revenue related to "certain promotional gift card and e-commerce transactions";

costs of goods sold caused by errors in "recording duty costs for certain inventory shipments";

errors in tracking prepaid expenses, and

certain other errors and adjustments.

The Company corrected the errors as a “little r” revision because, based on the Company’s analysis, the errors were both quantitatively and qualitatively immaterial. “Little r” errors are generally less visible and are easy to overlook because they do not require alerting the investors through filing an Item 4.02 of Form 8-K.

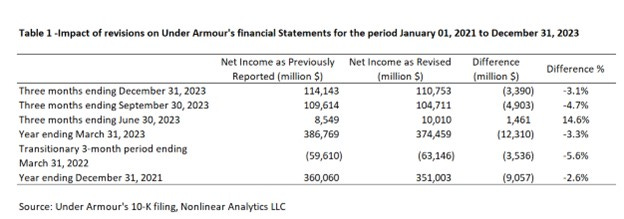

Looking at the initial and revised information provided by the company in its 10-K filing can give us a sense of the quantitative impact.

The impact on most affected periods was within 3-5% range, broadly supporting the Company’s conclusion that the restatement was quantitatively immaterial.

Now, let's turn to qualitative considerations. ASC 250 states that companies should consider the impact of the errors on executive compensation in evaluating the overall materiality. From PwC Viewpoint: